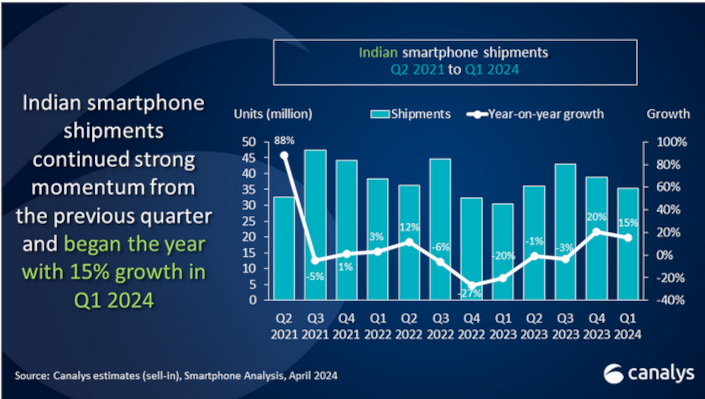

The Indian market grew 15% year-on-year in the first three months of 2024, Canalys said this was in part due to the lower base of the first quarter in 2023.

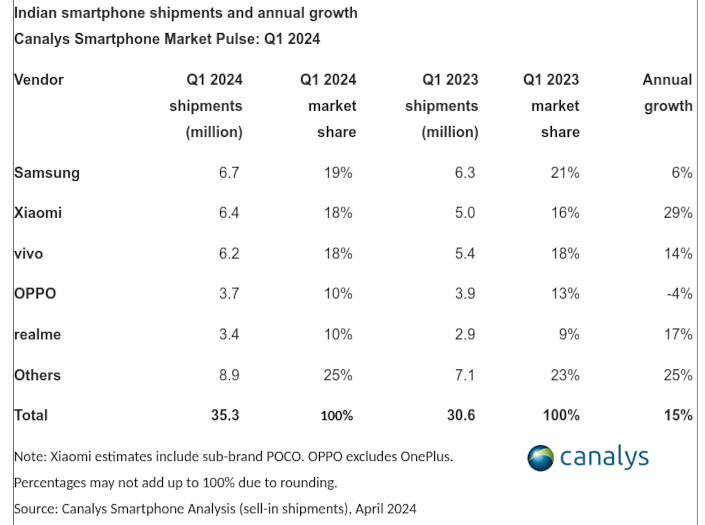

Samsung kept the top spot with a 19% share and 6.7 million units shipped. Xiaomi was second (6.4 million units) followed by vivo (6.2 million units), Oppo (3.7 million units) and realme (3.4 million units). The Oppo figures do not include OnePlus.

Canalys senior analyst Sanyam Chaurasia pointed out that while most brands achieved double-digit growth in 1Q, brands outside the top five continue to challenge the market share of leading players.

|

|

"Samsung’s latest flagship Galaxy S24 had a stronger volume than its predecessor, owing to lucrative pre-booking offers on upgrade value, Samsung Finance+ and extensive AI features marketing.

"Xiaomi saw a robust 1Q resurgence fuelled by the Redmi 13C 5G and Redmi Note 13 5G series, along with POCO's early launch of the X6 series.

"Oppo saw a modest decline, having streamlined its portfolio with fewer new releases in the mid-high price ranges. Out of the top five – Motorola, Infinix, and Apple achieved high double-digit growth, narrowing the market share gap from top players.

"Apple's growth was driven by its cash cow iPhone 15 model which received multiple price cuts and promotional deals on the e-commerce platform.”

The Indian Apple figures were in sharp contrast to the China market, where iPhone sales tumbled 19.1% in the first quarter of 2024.

Chaurasis added that mass-market brands were prioritising value-driven strategies in response to sluggish demand growth in the volume-driven segment.

“In 1Q, brands such as Xiaomi, vivo, and Oppo introduced their latest models — Redmi Note 13, V30, and the Reno 11 series — at a higher price compared to the models of the previous generation.

"Vendors are aggressively pricing their products to capitalise on the premiumisation trend fuelled by wider channel access and easy financing options. Price hikes are expected to continue as operational pressures rise due to higher component costs, despite import duty reductions on a few parts.

"Brands are also prioritising channel incentives and retail investments, driving costs up further. This year, brands will look to justify incremental pricing beyond the 5G capabilities. This will be mainly through design language, user experience and other integrated smartphone AIoT offerings.”

Chaurasia said emphasis on localisation in the Indian smartphone ecosystem had become inevitable.

“While in 2024 growth catalysts seem to be limited to just 5G device upgrades and premiumisation, vendors must focus on long-term strategies for share sustainability," he added.

"Amid the government localisation push, vendors must further focus on restructuring local distribution, leveraging local manufacturing partners and appointing Indian leadership.

"Additionally, they need to prioritise enhancing user experience and educating consumers for effective device engagement. Expanding into smaller cities, bolstering mainline retail, and building channel confidence will be crucial.”